What is a Capitalization Rate in Real Estate

If you are a real estate investor or dipping your toes into passive real estate investments, one of the first metric terms you'll encounter is a capitalization rate (or more commonly called a cap rate). While this metric is simple and can be a good indicator of a property's net operating income or value, how it's used can be confusing. Even more confusing can be the impact of rising and falling cap rates on real estate values (and your investment returns).

In this article, we’ll explore the full scope of the capitalization rate—what it is, how it’s calculated, the factors that influence it, and how to interpret its value. Whether you're assessing a commercial real estate fund or reviewing a multifamily syndication opportunity, a strong grasp of cap rates will empower you to make smarter, data-driven investment decisions.

What is a Cap Rate?

A capitalization rate, commonly referred to as the cap rate, is a financial metric used to evaluate the income-producing potential of a commercial real estate asset.

The cap rate expresses, as a percentage, the unleveraged annual return a property is expected to generate based on its existing income stream. It assumes the property is purchased entirely in cash, without the use of financing.

Cap rates are used to:

- Estimate an asset’s return profile relative to its value

- Compare income-producing properties within or across markets

- Assess relative risk and stability in real estate investment opportunities

- Derive market-based valuations from income performance

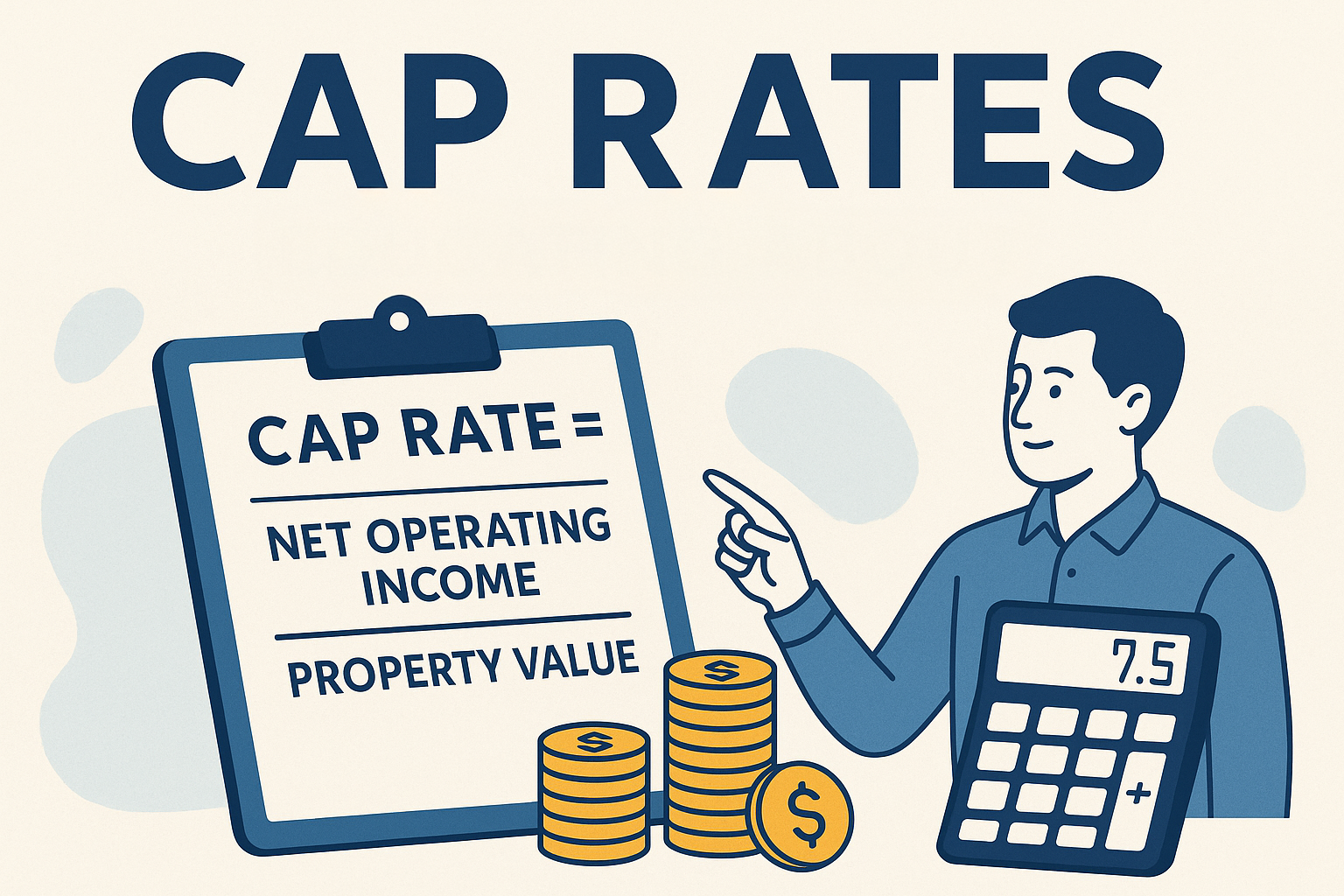

The Cap Rate Formula

The capitalization rate evaluates the relationship between a property’s income and the asset value. It is calculated using the following formula:

Net Operating Income (NOI)

Net Operating Income is the annual income generated by the property after deducting all operating expenses, but before subtracting any debt service (mortgage payments), capital expenditures, depreciation, or income taxes. Operating expenses typically include:

- Property management fees

- Property taxes

- Insurance premiums

- Repairs and maintenance

- Utilities (if paid by the owner)

Current Market Value

The market value represents the price the property would command under current market conditions. It may differ from the actual purchase price or asset value, particularly in off-market or distressed transactions. The market value should reflect the property's income potential relative to other similar assets.

Example of a Cap Rate Calculation

If an investment property generates $250,000 in annual NOI and has a current market value of $3,125,000, its cap rate is:

$250,000 / $3,125,000 = 0.08 or 8%

An 8% cap rate means the property generates an 8% return annually on its market value, assuming consistent income and no leverage.

Cap rates reflect the market’s view of a property's income reliability and risk profile. Properties in prime locations with stable cash flow and low turnover often exhibit lower cap rates, while assets with operational challenges or uncertain income streams tend to have higher cap rates. Interpreting this figure in context is essential for effective investment analysis.

How Cap Rates Are Used in Real Estate Investment Analysis

The capitalization rate serves several roles in real estate investment analysis. It is commonly used to compare properties, assess changes in market value, estimate asset pricing, and approximate income-based returns. Each of these applications is outlined below.

Cap Rates Used to Calculate Property Values

Cap rates are a critical tool in property valuation. The following formula is used to estimate a property’s value based on market-derived cap rates:

A capitalization rate valuation method is frequently used by appraisers, underwriters, and investors to assess whether a property is priced in line with similar assets in the market.

Cap Rates Used to Calculate Expected Returns

Cap rates also function as an indicator of a property’s expected annual net operating income. When an investor acquires a property in cash and income/expenses are assumed stable, the cap rate provides an estimate of the annual yield.

It is important to note that the cap rate is not a comprehensive measure of investment return. Unlike metrics such as internal rate of return (IRR) or cash-on-cash return, the cap rate:

- Does not reflect the financing structure

- Omits capital expenditures

- Ignores tax benefits and depreciation

- Excludes any future appreciation assumptions

Therefore, cap rate should be interpreted as an initial yield, useful for screening and comparison, but insufficient for full return analysis. Passive investors should view it as a starting point for evaluating income strength, not a definitive measure of total performance.

Cap Rates Used to Compare Properties

One of the most common uses of the capitalization rate is to compare investment properties across different markets, asset types, and investment scenarios. The cap rate offers a standardized measure that enables real estate investors to quickly evaluate whether a property is priced appropriately in relation to its income-generating performance. Since the cap rate reflects the relationship between a property’s net operating income (NOI) and its price, it allows investors to evaluate which asset offers a more attractive yield relative to price.

Consider two comparable apartment buildings in the same submarket. Property A is listed for $5 million, and Property B is listed for $7 million. Suppose Property A generates $350,000 in net operating income, while Property B produces $420,000 in NOI.

- Property A Cap Rate: $350,000 ÷ $5,000,000 = 7.0%

- Property B Cap Rate: $420,000 ÷ $7,000,000 = 6.0%

At first glance, Property A offers a higher cap rate, suggesting it generates more income per dollar of value than Property B. This could imply a more attractive initial yield, but it may also signal higher perceived risk, operational inefficiencies, or outdated physical condition. Alternatively, it could signal that the seller of Property B is overambitious with their sale expectations.

Cap rates help passive investors compare relative value among opportunities within the same asset class. They distill income performance into a single figure that highlights which property may offer better returns, assuming similar conditions. However, investors must still analyze underlying factors such as tenant quality, expense structure, and future upside before drawing conclusions.

Cap Rates Used to Communicate Value Changes

Cap rates are sensitive to changing market conditions and are often used to signal shifts in property value. One important concept in this context is cap rate compression, which occurs when market cap rates decline. This phenomenon typically reflects increased investor demand, lower interest rates, or a favorable perception of reduced asset risk.

What is Cap Rate Compression?

Cap rate compression is term used when cap rates get lower (such as when market cap rates go from 6% to 5%). When cap rates compress but NOI remains constant, the value of the property increases. Lower cap rates tend to indicate higher property values. This relationship is why declining cap rates are often associated with appreciation in real estate pricing.

What Is Cap Rate Expansion?

Cap rate expansion is the opposite scenario, when market cap rates increase. This shift typically reflects changes in macroeconomic or property-specific factors that elevate perceived risk or reduce investor confidence. When cap rates expand, it indicates that property values are dropping.

Common causes of cap rate expansion include:

- Rising interest rates

- Economic uncertainty or local market instability

- Reduced demand for a specific asset class

- Deterioration in tenant quality or lease stability

- Oversupply in the market or regulatory risk

Cap Rates Used as a Risk Assessment Tool

Cap rates can be used to assess risk, or more accurately, they should reflect how the market perceives the risk of a property. In general, the higher the cap rate, the more risk is assumed to be tied to the deal, which is why you'll often see higher cap rates in more rural markets or riskier asset classes (like in today's office market). A lower cap rate usually reflects lower risk (as we see in core and core plus multifamily), usually because the property is in a strong location, has stable occupancy, or is newer and requires less maintenance.

For example, if two properties generate the same net operating income, but one has a higher cap rate, then its purchase price is lower. The market is signaling that this asset comes with more uncertainty, maybe due to location, older condition, or less reliable tenants. On the flip side, a property with a lower cap rate is likely more expensive relative to its income, because it's seen as more stable or secure.

This risk-return relationship is important for real estate investors. While a higher cap rate might look attractive because it suggests stronger income relative to price, it’s important to dig deeper and understand what’s driving that number.

If you’re evaluating a deal with a noticeably higher cap rate, consider asking:

- Is the property in a less desirable or declining location?

- Are there issues with the current tenants or lease terms?

- Does the building require major repairs or capital expenditures?

- Is there high tenant turnover or vacancy risk?

- Are local market conditions affecting rental demand or property values?

- Is the property being sold at a discount due to distress or poor management?

- What is the sponsor's business plan to mitigate risk?

How Cap Rates Are Used as a Marketing Tool

Cap rates appear front and center in property listings, investment summaries, and offering memoranda. For sponsors and brokers, cap rates offer a simple way to draw attention to a property's income potential. For investors, these numbers can look persuasive at a glance, but it’s worth understanding how they’re framed.

The cap rate shown in marketing materials doesn’t always reflect current performance. In most cases, it’s based on future income projections, not actual financials. Additionally, marketing materials might feature different versions of a cap rate. These are some of the most common:

- Pro Forma Cap Rate: Based on projected NOI after anticipated improvements. Common in repositioning strategies and renovation plans.

- In-Place Cap Rate: Based on the current NOI using actual rents and expenses. This version reflects what the property is earning right now.

- Market Cap Rate: Derived from comparable property sales in the same location and asset class. Used to benchmark a property’s pricing.

- Going-In Cap Rate: Uses NOI at acquisition to show the buyer’s expected initial yield based on purchase price.

Because cap rates in marketed materials are usually pro forma cap rates, it's important for investors to know what that means. Projections could include expected rent growth, reduced operating expenses, or projected property taxes, but that doesn't necessarily mean that projections are correct, and that creates risk. While sponsors should take on the due diligence of reviewing projections and analyzing the market, investors should ask questions about the cap rate (especially if using it as investment criteria) and what needs to be achieved for that cap rate to become a reality.

When reviewing a deal, always ask which version of the cap rate you're looking at. Numbers based on forward-looking assumptions can look strong on paper but may come with execution risk. Knowing the source of the cap rate helps you put the rest of the investment package in perspective.

Factors That Influence a Property’s Cap Rate

Cap rates are not fixed values; they fluctuate based on a range of variables tied to both the individual property and broader market conditions. Investors use cap rates as a reflection of perceived risk and expected income performance.

Property Type

Different asset classes tend to carry different cap rate ranges due to their unique risk profiles and operational dynamics. For example:

- Industrial properties often have lower tenant turnover and long-term leases, which may result in lower cap rates.

- Short-term vacation rentals can generate high income but often come with higher volatility and regulatory risk, leading to higher cap rates.

Location and Local Economic Conditions

Location remains one of the most important drivers of cap rate variation. Properties in core, supply-constrained urban markets often trade at lower cap rates due to consistent demand and strong economic fundamentals. In contrast, tertiary markets or economically unstable regions may exhibit higher cap rates, reflecting elevated uncertainty and limited buyer pools.

Rental Income and Rental Rates

A property’s gross rental income and the trajectory of local rental rates play a critical role in shaping cap rate perceptions. Properties with strong in-place rents and potential for growth may command lower cap rates. Conversely, stagnant or declining rent potential may push cap rates higher, as future income gains appear limited.

Operating Expenses and Capital Expenditures

Higher operating expenses (property taxes, insurance, utilities, and management fees) can lower net operating income, thus influencing the perceived return on investment. Additionally, expected or recurring capital expenditures, such as roof replacements or system upgrades, may elevate the cap rate by signaling greater ongoing financial commitment.

Property Age, Tenant Stability, and Income Fluctuations

Older buildings may have higher cap rates due to anticipated maintenance costs or outdated features. Similarly, properties with unstable tenants, short lease terms, or inconsistent cash flow often carry a risk premium reflected in higher cap rates. On the other hand, newer assets with long-term, creditworthy tenants may support lower cap rates due to reduced operational risk and stable income streams.

What a High or Low Cap Rate Indicates in a Real Estate Investment

Cap rates serve as a market signal for both income potential and risk exposure.

A higher cap rate generally reflects a property that offers a higher return on investment, assuming stable net operating income (NOI). However, this return often comes with elevated risk. Contributing factors may include:

- Weaker location fundamentals

- Unstable tenant base or lease rollover exposure

- Deferred maintenance or outdated infrastructure

- Volatile income patterns or limited rent growth potential

Higher cap rates are common in secondary and tertiary markets, or in asset classes such as hospitality or short-term rentals, where income predictability can vary.

A lower cap rate usually indicates lower perceived risk and more predictable income streams. Properties in this category tend to have:

- Prime locations with strong tenant demand

- Long-term leases with creditworthy tenants

- High-quality construction and minimal deferred maintenance

- Favorable economic indicators in the surrounding area

These assets often appeal to conservative investors seeking stable, long-term income, even if that comes with a lower initial yield.

How Cap Rates Impact Negative vs Positive Leverage

Leverage is the use of debt in real estate investments. It can amplify returns, but it also introduces risk. The terms positive and negative leverage reflect the relationship between a property's cap rate and the interest rate on its financing.

Positive Leverage

Positive leverage occurs when the cap rate exceeds the interest rate on the loan. In this scenario, the investor is borrowing at a lower cost than the unleveraged return produced by the property’s income. As a result, the use of debt increases the cash-on-cash return and enhances total yield.

Example:

- Cap Rate: 7.0%

- Interest Rate: 5.0%

- Leverage spreads the return, improving the investor’s equity performance

This form of leverage is often sought in stable markets with strong income performance and moderate borrowing costs. Some passive investors will only invest in real estate when the deal has positive leverage.

Negative Leverage

Negative leverage happens when the interest rate on debt exceeds the property’s cap rate. In this case, the cost of borrowing is greater than the return the asset generates on a cash basis. Using leverage in this environment reduces the return on equity and increases financial risk.

Example:

- Cap Rate: 5.5%

- Interest Rate: 6.5%

- Debt service outpaces income yield, eroding investor returns

Negative leverage is more common in high-interest-rate environments or when properties are acquired at aggressively low cap rates. It may be justified in specific scenarios, such as a short-term hold with strong appreciation potential, but generally signals a riskier investment profile. Some passive investors will not invest in a deal if it has negative leverage, which can make finding an investment difficult.

Implications for Passive Investors

Sponsors may present appealing projected returns, but those projections depend heavily on whether the debt structure enhances or diminishes the income performance of the property. Passive investors should review:

- The spread between the cap rate and the interest rate

- The sponsor’s assumptions about rent growth and refinancing

- The impact of leverage on cash flow and risk tolerance

Properly structured leverage aligned with a favorable cap rate can boost returns. However, misaligned cap rate and debt terms can introduce significant downside, especially in volatile or compressing markets.

Limitations of Cap Rate in Investment Decisions

While the cap rate is a widely used and valuable tool for evaluating real estate investments, it is not the only metric you should rely on and it has limitations. Relying on it in isolation will lead to an incomplete or misleading picture of a property's financial profile and future potential.

1. Does Not Account for Leverage or Financing

The capitalization rate calculation assumes a cash purchase and does not reflect the impact of debt. As such, it does not provide insight into cash-on-cash return, debt service coverage, or the effect of positive or negative leverage. Investors using financing must look beyond the cap rate to understand how debt will influence returns.

2. Ignores Tax Implications and Depreciation Benefits

Cap rate calculations do not incorporate tax treatments, including depreciation, amortization, or investor-specific tax brackets. These variables can significantly impact after-tax return, particularly for passive investors in syndications where pass-through tax advantages may be a central part of the value proposition.

3. Excludes Future Capital Improvements and Upside Potential

Cap rate reflects current or in-place performance and does not capture the value of future enhancements. For value-add or opportunistic deals, where the investment thesis depends on increasing rents, renovating units, or repositioning the asset, the cap rate provides limited insight into total return potential.

4. Static View of Income with a Short-Term Perspective

Cap rate is based on a single year of NOI, offering a snapshot rather than a full performance picture. It does not project income growth, expense escalation, or changes in market conditions over the hold period.

5. Difficult to Use to Compare Properties in Different Markets

Because cap rates are deeply tied to local market fundamentals, comparing properties in different geographic regions using cap rates alone is problematic. A 6% cap rate in a stable primary market may reflect a very different risk/return profile than the same figure in a less liquid or more volatile secondary market.

How Passive Investors Should Use Cap Rates

A cap rate is useful to evaluate commercial real estate deals, but it's also an incomplete tool. It provides a starting point for evaluating deals and understanding how the market prices income-producing properties, but it should be interpreted carefully within the context of a sponsor’s overall strategy.

Use Cap Rate as a Screening Metric

Cap rates offer a quick snapshot of how much income a property generates relative to its value. Passive investors can use this figure to compare multiple opportunities and filter deals that meet their income and risk preferences.

- Higher cap rate → potentially higher yield and risk

- Lower cap rate → potentially lower yield and greater stability

Evaluate the Spread Between Cap Rate and Interest Rate

Compare the cap rate to the cost of debt. A favorable cap rate spread (cap rate above interest rate) may indicate positive leverage, which can enhance equity returns. A narrow or negative spread suggests increased financing risk.

Consider Cap Rate Trends in the Target Market

Cap rates fluctuate based on market conditions. Passive investors should pay attention to whether cap rates in the target market are compressing or expanding, as this will affect both acquisition price and exit assumptions.

Questions to Ask Real Estate Sponsors About the Cap Rate

- Is the cap rate based on actual or projected income?

Ask whether it reflects current operations or a future business plan. - What specific expenses were included in the net operating income calculation?

Some marketing materials may leave out property management, reserves, or insurance. - How does this cap rate compare to other properties in the same market and asset class?

Market comps can reveal whether a deal is aggressively priced or fairly valued. - What assumptions are built into the cap rate if it's based on pro forma numbers?

Look for assumptions about rent growth, vacancy, and expenses. - Has the cap rate changed recently, and why?

Cap rate compression or expansion often reflects larger market trends like interest rates or local demand shifts. - What is the exit cap rate assumption?

This affects resale projections and future returns. It should be more conservative than the entry cap rate. - Does the cap rate reflect the risks associated with this specific property?

For example, location, tenant quality, lease length, and deferred maintenance.

Cap Rates Part of a Bigger Picture

For real estate investors (both passive and active), cap rates are most effective when used in combination with other financial metrics such as IRR, cash-on-cash return, and equity multiple. Just as importantly, they should be considered alongside a thorough evaluation of the sponsor, including their track record, transparency, and operational discipline.

Before making a commitment, ask the right questions, dig into the assumptions behind the numbers, and make sure the investment aligns with your personal goals.

Looking for a more complete view of your investment options? Invest Clearly makes it easy to find verified investor reviews and gain real insights into sponsor performance and communication, so you can invest with confidence and clarity.

Written by

Invest ClearlyOther Articles

What Is a Capital Stack?

Every real estate deal needs funding, which is why real estate syndication and private equity investments have become so widespread. However, where that money comes from and in what order it gets repaid isn't random. It's structured carefully, layer by layer, in what's known as the capital stack.

Power of Community in Passive Investing | Brian Davis

Brian Davis shares how Spark Rental's co-investing club vets deals, evaluates operators, and helps investors build passive income

Evaluating Real Estate Sponsors: The Role of Social Proof in Investment Decisions

This article explores the role of social proof in evaluating real estate sponsors, the risks of relying solely on past returns, and the dangers of influencer marketing in investment decision-making.

What is a Syndication Real Estate Investment?

A real estate syndication is a common investment structure that pools capital from multiple investors to acquire and manage larger commercial real estate assets.

Using AI, Community, and Transparency to Build a Better Investment Firm with TJ Burns

TJ Burns, founder of Burns Capital and ex-Amazon engineer, joins the Invest Clearly Podcast to break down the real challenges of raising capital and building long-term LP trust.

The 'Institutional' Tax: Are You Paying a Premium for Prestigious Partners?

For LPs navigating an increasingly complex private real estate landscape, understanding when institutional backing genuinely adds value - and when it merely adds cost - is vital to optimizing your allocation strategy and maximizing risk-adjusted returns.